Is Australia’s property market really a precarious house of cards waiting to topple?

There’s a property debate raging at present – some say the future for property is bright while others suggest our markets are set to crash.

After a number of boom years, especially in the Sydney and Melbourne property markets, we’ve entered a more mature stage of the property cycle, and obviously, it would be good to know who’s right if you are considering investing in property, or about to buy a home.

Click here to view the video on YouTube.

But remember there is not one property market around Australia

Our markets are fragmented – not only is each state at its own stage of its property cycle, but within each state different segments of the markets are behaving differe ntly.

ntly.

So it doesn’t really make much sense to say the “Australian property market” will crash.

Interestingly I’ve heard many theories as to why the property bubble will burst.

Some doomsayers are predicting a property crash because house prices have risen too high and are now unaffordable.

Others suggest we have taken on too much debt both personally and as a nation.

However, just because houses prices are high or unaffordable to some, doesn’t mean we have a property bubble.

In fact, I’m going to give you seven good reasons why the property markets won’t crash, but first…

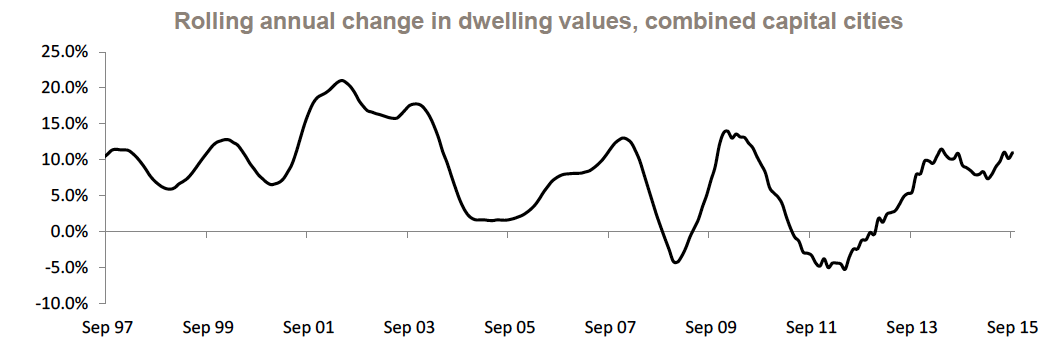

Let’s look at how property markets corrected in the past.

To understand what’s ahead, let’s look at what happens when property markets got ahead of themselves in the past.

![[Imported] WP Advertize it Free Strategy ad 10 July 2014 (Desktop #44800)](http://propertyupdate.com.au/wp-content/uploads/2014/07/m-propertyinvestors-18July2014.png)

Sydney had a terrific boom between 2001 and February 2004.

In fact it was one of the best performing property markets between 1996 and 2004, helped in part by the excitement related to the Olympic Games.

After this boom the Sydney property market corrected.

It didn’t collapse – it just corrected – with values falling from peak to trough by -9.3% and this fall took a total of 23 months to play out.

Of course not all parts of the Sydney market dropped in value equally – some areas held their values well.

And even in the regions where values fell, property prices didn’t plummet – they gently followed a downward path.

The doomsayers were out then also, but just look at where Sydney property prices are today.

A similar pattern occurred in Brisbane and Perth where values peaked in February 2008 after a long boom in both cities pushed their house prices well above the average national price growth.

Again property prices didn’t collapse – they just sauntered along allowing the fundamentals to get back into alignment.

Much the same happened in the early 1990’s when we experienced “the recession we had to have.”

After the remarkable property boom of the late 80’s, interest rates rose to peak at around 17% and the property markets around Australia stalled.

But once again they didn’t collapse.

They just flat lined for a few years as affordability, supply and demand other economic fundamentals caught up.

And when property prices peaked in late 2010, the last time the RBA pushed up interest rates, property prices gently eased in our major capital city markets – they didn’t plummet.

Source: Corelogic

The only time Australian property values dropped significantly (albeit for a short time) was after the Second World War and during the Great Depression.

In the 1940’s house prices dropped 17% over a two year period but then jumped back and grew strongly for many years after that.

Property values also dropped during the Great Depression when unemployment was high, but times are different today.

No one is suggesting that Australia is heading for a depression.

Sure our economy is slowing a little, but it’s still the envy of most developed nations.

That’s why talk of a property market collapse is nonsense.

Why don’t Australian property markets collapse?

Well some do!

Just look at the mining towns where the values of some properties have fallen by over 50%.

Or some holiday destinations like the Gold Coast.

But here’s why…

The mining towns where driven to dizzy heights by speculators and the Gold Coast was also driven more by speculation than by underlying supply and demand fundamentals.

The large fall in prices there was because there was too much developer stock on the market.

But my point is that, in general, our capital city property markets don’t collapse because they are illiquid.

People don’t sell up their homes just because interest rates rise or when times get tough.

So what could cause a property market collapse?

Looking at what has happened in the past, both here and overseas, the factors that could make our markets to collapse (rather than correct) are:

1. A depression or a severe recession– no one is suggesting this is likely in the near future.

2. Unemployment levels so high that a mass of people can’t afford to keep their homes.

Again this is unlikely to occur with unemployment levels being as low as they are.

3. Interest rates rising to levels that cause home owners to default on their mortgages.

Hopefully the RBA won’t allow this to happen.

4. A huge oversupply of properties because developers have built too many.

We’re currently seeing this in the overheated inner city off the plan market segments, especially in Melbourne, Brisbane and Perth.

5. Credit market illiquidity or a credit squeeze. Currently APRA are trying to slow down the growth of our property markets to underpin the banking system, but they’re not looking to choke the markets.

That wouldn’t be good for anyone.

Why property won’t crash

There are a number of reasons why we won’t see major falls in home prices in our capital cities any time soon.

We have:

1. Robust population growth fueled by immigration and to a lesser extent strong natural population growth.

While immigration levels have dropped, we’re still growing at a faster rate than any other country in the developed world.

2. A healthy economy that, while slowing a little, will continue to perform at a level that is the envied by of much of the Western world and will create jobs for anyone who wants one.

3. A sound banking system with reasonable interest rates, tight lending practices and low default rate.

4. Business confidence is rising as we seem to have a stable government at both the Federal and State levels.

5. Consumer confidence has been rising since Malcolm Turnbull was elected Prime Minister.

6. A healthy level of household debt.

Sure we are borrowing more, but the debt tends to be in the hands of those who can afford it.

Many Australians are saving more, taking on less credit card debt and paying off their mortgages faster than they need to which improves the state of their personal finances.

This in turn reduces the risk of house prices collapsing if interest rates rise or the economy hits a speed bump.

7. A culture of home ownership – seventy per cent of us own or are paying off our homes.

In contrast to some overseas markets Australians have high equity in their properties and a conservative debt position.

In fact half of all homes have no debt against them.

There’s no sugar coating it…property price growth will slow in 2017

Decreasing affordability, changing sentiment and oversupply in several sectors such as CBD and off the plan apartments will create a volatile mix that will fragment and slow our property markets – moving some from a seller’s to a buyer’s market.

This is already evident with falling auction clearance rates particularly in the Sydney property market.

Yet there is still a large demand for housing – people are still getting married, having babies, getting divorced and coming from overseas.

And if they can’t afford to buy their homes they are going to rent and this will force rentals up.

So what’s ahead?

As Australia’s economy bumbles along I can see little wages growth over the next year or two, but I do see interest rates rising sometime in 2017 and both these factors will  affect some suburbs more than others.

affect some suburbs more than others.

What I mean by this is that rising rates are likely to affect suburbs that are more interest-rate sensitive like blue-collar areas, regional locations and first-time buyer locations.

On the other hand, property values are likely to increase in the more affluent, gentrifying middle ring suburbs of our major capital cities where the locals’ income is less dependent on CPI rises in wages and where rising interest rates are less likely to have an impact on disposable incomes.

So my top picks for suburbs that will outperform would include suburbs where people have higher disposable incomes and are able to, and prepared to, pay a premium to live there the because of the amenities in the area.

Property price growth in Sydney will likely slow to around 5% over the year ahead and Melbourne prices should grow a little more than this (+7%).

Prices will fall a little more in Perth and Darwin as the mining boom continues to unwind, while Hobart is likely to see continued moderate property growth, but the Brisbane property market should start to pick up further as it plays catch up rising around 7% over the year.

And I can’t really see a reason for regional or mining town real estate to have much capital growth.

There is no influx of new people moving to these regions little to strengthen their economies and investors are no longer buying up big in these regions.

But rest easy – there won’t be a property market crash in our capital cities.

WHAT WILL YOU DO IN 2017?

If you’re looking for independent property investment advice to help you become financially independent, no one can help you quite like the independent property investment strategists at Metropole.

We’ll help you cut through the clutter of mixed property messages.

We’ll help you cut through the clutter of mixed property messages.

Remember the multi-award winning team of property investment strategists at Metropole have no properties on the market to sell, so their advice is unbiased.

Whether you are a beginner or a seasoned property investor, we would love to help you formulate an investment strategy or do a review of your existing portfolio, and help you take your property investment to the next level.

Please click here to organise a time for a chat.

OR CALL US ON 1300 20 30 30.

When you attend our offices in Melbourne, Sydney or Brisbane you will receive a free copy of my latest 2 x DVD program Building Wealth through Property Investment in the new Economy valued at $49.

No comments:

Post a Comment